How Scenario Planning for Tax Forecasts Should Work in 2021

Scenario planning is an increasingly important way for multinational enterprises to operate effectively in an uncertain and unpredictable world. It helps them to react to small and large market fluctuations in the most cost-effective and strategic manner, modelling ”what-if” situations according to both known and unknown information.

Rapid advances in technology are helping to transform the way organizations carry out scenario planning, allowing them to adapt a continuous planning mindset to other areas of finance, such as tax. As a result, tax teams are able to leverage their increased planning capabilities to provide the insights senior leaders need to make more informed strategic decisions across their organizations.

- Understand how to reduce tax errors and improve productivity

- Learn how to enable complex planning and forecasting processes

- Discover our top tips for achieving tax agility in 2020

Predicting estimated tax returns is a great example of how tax teams can use technology to become more agile and insightful when running different scenarios. This is the view of Jamie Eagan, VP of Product Management of Longview products at insightsoftware, who spoke at a webinar held on Sept. 16.

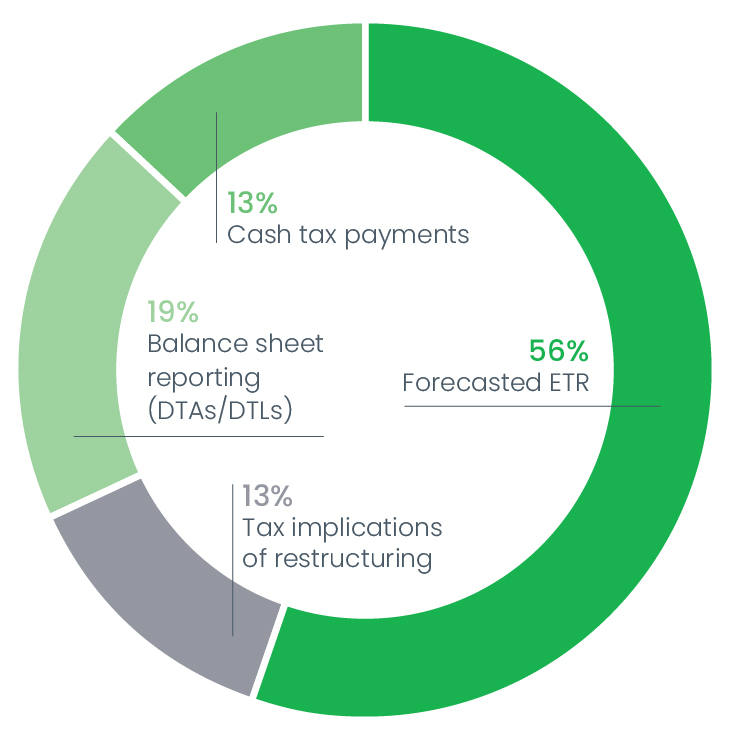

In this webinar, attendees responded to a poll asking which areas of long-term forecasts are of most interest to them. The results were as follows, demonstrating the importance of scenario planning in building an accurate view of the many different aspects related to future tax liabilities*:

Forecasted ETR: 56%

Balance sheet reporting (DTAs/DTLs): 19%

Cash tax payments: 13%

Tax implications of restructuring: 13%

Planning different types of scenarios

Because there are so many factors that contribute to overall tax forecasts, it’s important to run several different types of scenarios to account for these variables.

A good place to start is with a best case/worst case pair of outcomes. As Kathryn Abate, Presales Director EMEA of Longview Products at insightsoftware, explained, by plotting the two extremes of an event, it’s possible to find a midpoint that gives you three views of a situation, including the most pragmatic position between those two outcomes.

A second approach to structuring scenarios has been outlined by finance consultants. The fast-changing environment in which businesses currently operate means that it may be necessary to undertake two types of scenario planning—one for recurring elements and one for discrete events, such as product launches or crises, including the current pandemic. Having access to these different types of scenarios, and looking at them all holistically, can be very helpful when predicting or anticipating change in an organization’s bottom line.

It’s important to build a 360° view of data being used in any given scenario, including external sources as well as forecasts from the finance team. Data from finance need to be as accurate as possible, but also at the level of granularity that tax teams need, that is, at a legal entity rather than a country level.

Ideally, tax teams should be able to update data used in their scenario planning dynamically, that is, by plugging in the most up-to-date operations and consolidated finance data in line with ongoing events. Few would have built a scenario in March that took into account the actual impacts of COVID-19, for example, so forecasts need to be adjusted accordingly in rapidly evolving situations.

Scenarios should also include and point out exceptional items, which are charges incurred that must be noted separately in financial reports, as well identifying the underlying items, which are generally more predictable and under control. “Exceptional items can be stripped out of headline numbers if need be, while exceptional items from the past may now have become underlying items,” said Abate.

How to achieve your goals in scenario planning

Step 1

The first stage when planning a new scenario is to understand the data that are required. “You have to start by working out what is useful and material in a scenario and what isn’t,” said Eagan. “This can include historical data as well as data that have seen huge changes because of changing market conditions, such as travel and entertainment. It’s also useful to understand corporate initiatives, including spending freezes, that may impact future scenarios.”

Step 2

The next stage is to build the scenarios themselves, said Abate. “It’s tempting to keep trying out different types of scenario planning, perhaps using Excel and pressing ‘Save As’. The problem is that you will end up with so many different spreadsheets that you lose sight of what you’re trying to model.”

By using dedicated software instead of spreadsheets for scenario planning, tax teams can bring huge efficiencies to the process. But be warned that planning needs to involve more than just the software itself, because while applying tools to broken processes or inaccurate data will mean manual labour is reduced, there may also be a risk of making the wrong forecasts. “You have to look at this in the round,” she said. “It needs to involve processes, people, data, and governance.”

Step 3

Once all of this is addressed, organizations can move to a more frequent cadence of scenario planning and reporting, migrating from quarterly to monthly forecasts based on the updated scenarios and underlying data. The key priority at this stage is to focus on the most important goals for the business, notably the elements that will materially impact performance, such as the price of components, changing tax rates, or headcount.

“One of the reasons many businesses stick with a quarterly forecast is that tax teams have limited time and resources to work on these reports,” said Eagan. “To make best use of the time available, teams can prioritize the key levers that make the biggest differences. It may be that you only have to make updates on these limited numbers of indicators; you don’t need to reinvent the wheel each time, but just take periodic snapshots to demonstrate progress.”

Even so, the key levers and periodic snapshots can become easier to understand and update by ensuring that the data are sourced in a correct format and level of granularity. To do so, she detailed three main tactics:

- Improve communications between tax and finance – It may be that finance already has the data needed, but doesn’t know they are required by the tax team

- Make process changes, taking a step back to focus on how to build a more effective way to capture the data needed

- When it’s impossible to make wholesale process change, work to change expectations from the business on what is ”nice to have” versus what is ”must have” information

The advantages of Longview Tax

Using software such as Longview Tax, it’s possible to gather relevant data quickly and easily, compare current and historical scenarios, consider forecast and actual performance, and learn from successful forecasts so that the process can continue to improve moving forward. Tax forecasts are automatically updated when adjustments are made and regular forecasts can be shared in a graphical format with key decision-makers.

Find out how Longview Tax helps you plan for the future

As tax regimes and global trading conditions continue to change in new and unexpected directions, keeping a careful eye on tax liabilities will be more vital to the financial health and compliance requirements of large multinationals than ever before. The role of software to underpin tax planning will only increase in importance.

See more about Longview Tax and book a free demo

*Values have been rounded to the nearest percent, which may result in a final total that exceeds 100%.